Overview

The Federal Reserve announced that it was expanding the scope of the Municipal Liquidity Facility (MLF) by permitting cities with populations in excess of 250,000 residents and counties with populations in excess of 500,000 residents to participate. The Federal Reserve also announced which cities and counties qualify for the borrowing and how much they can borrow. Below is a quick summary of the program.

- Eligible issuers are states and cities with more than 250,000 residents and counties with more than 500,000 residents that were rated at least BBB-/Baa3 as of April 8, 2020, that certify in writing they are unable to secure adequate credit from banking institutions and are not insolvent.

- The principal amount of notes cannot exceed 20% of the general revenue from the issuer’s own sources and utility revenues; interest rates will be determined in the future; the notes must mature within three years; and the notes must be general obligations or otherwise backed by tax or other specified governmental revenues of the issuer. An opinion of bond counsel is required to issue the notes.

- Proceeds of the notes must be used to help manage the cash flow impact of income tax deferrals resulting from an extension of an income tax filing deadline; potential reductions of tax and other revenues or increases in expenses related to or resulting from the COVID-19 pandemic; and requirements for the payment of principal and interest on obligations of the relevant state or eligible city or county. Proceeds of the notes may also be used to pay costs of issuance.

Background

When the Federal Reserve announced a MLF designed to support the flow of credit and liquidity to state and local governments during the COVID-19 pandemic, there was just one problem. The MLF was limited to states, and cities and counties with populations in excess of 1 million and 2 million people, respectively. This obviously excluded a lot of cities and counties that need assistance. After continued discussion, on Monday, April 27, the Federal Reserve announced that cities and counties with populations in excess of 250,000 and 500,000 people, respectively, are eligible to participate in the MLF. The Federal Reserve also extended the permitted maturity of the notes by another 12 months to 36 months and extended the initial duration of the program from September 30, 2020 to December 31, 2020. While the Federal Reserve expanded many aspects of the program, it tightened others. The Federal Reserve also released FAQs that clarified many aspects of the MLF. What follows is a general discussion of the revised MLF and the FAQ.

General Discussion

The MLF permits a special purpose vehicle (SPV) to purchase tax anticipation notes (TANs), tax and revenue anticipation notes (TRANs), bond anticipation notes (BANs), and other similar short-term notes from states and cities and counties with populations in excess of 250,000/500,000 people. Only states and cities and counties that were rated at least BBB-/Baa3 as of April 8, 2020, by two or more of Moody’s, S&P or Fitch may issue notes pursuant to the program, provided that any issuer that was downgraded below this threshold after April 8, 2020, must be rated at least BB-/Ba3 by two or more of Moody’s, S&P or Fitch as of the date its notes are sold to the SPV. Additionally, only states, cities and counties that can certify in writing that they are unable to secure adequate credit accommodations from other banking institutions and that they are not insolvent are permitted to sell notes pursuant to the program.

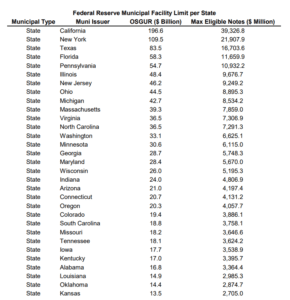

The principal amount of the notes cannot exceed 20% of the general revenue from the issuer’s own sources and utility revenues as reported by the U.S. Census Bureau. The Federal Reserve has computed the maximum amount of notes permitted to be sold by each eligible issuer to the SPV. Each issuer must pay an origination fee of 10 basis points of the principal amount of its notes sold to the SPV. The Federal Reserve is still determining the appropriate interest rate for notes, but it will be at a premium to the market rate in normal circumstances that will be based on the issuer’s long-term rating plus a spread over a publicly available benchmark or index. The term of the notes cannot exceed three years and may be prepaid at any time at par. The notes will be required to be general obligations of the issuer or otherwise backed by tax or other specified governmental revenues of the issuer. Finally, the SPV will require an opinion of bond counsel that the notes are valid, enforceable and binding upon the issuer under applicable state and/or local law.

Proceeds of the notes must be used to help manage the cash flow impact of income tax deferrals resulting from an extension of an income tax filing deadline; potential reductions of tax and other revenues or increases in expenses related to or resulting from the COVID-19 pandemic; and requirements for the payment of principal and interest on obligations of the relevant state or eligible city or county. Proceeds may also be used to pay costs of issuance of the notes and paying the 10 basis point origination fee.

Issuers with questions about the MLF may contact the Federal Reserve or any Frost Brown Todd Finance attorneys who serve as bond counsel and routinely deliver the kinds of opinions required to participate in the program, including Denise Barkdull, David Rogers, Steve Sparks, Laura Theilmann.