The choice of entity decision is a critical step in every company’s life cycle. At its onset, a business’s owners must decide where the business is going to be formed and what type of business entity it will be.

Here in the United States, the common business entity types include corporations (whether taxed as “C” or “S” corporations), LLCs, and partnerships. These different entity types bring different state law governance rules, which might make one entity type more advantageous than the other for state law purposes. Also, different entity types carry different tax consequences at the federal, state, and local level, which must be kept in mind.

Business owners and advisors might prefer to incorporate in any one state for different reasons. Businesses are often formed in the jurisdiction in which they are headquartered or operate primarily. Delaware is a popular state of formation because of its mature corporate law and court system. Venture capital and private equity backed companies typically choose to operate as Delaware entities.

After its formation, a business may need or want to change its entity type and/or place of formation. Such need or desire may be caused by changes in ownership, changes in investor demands, changes in tax or corporate laws, or changes in growth and exit strategies, among other business changes.

One useful tool that businesses and practitioners can utilize to restructure business entities on a tax-free basis as they adapt to changing circumstances is the F Reorganization under Internal Revenue Code (I.R.C.) § 368(a)(1)(F). The I.R.C. defines a F Reorganization as “a mere change in identity, form, or place of organization of one corporation, however effected.”[1] This mere change can be accomplished in many ways and for different reasons. This article will discuss the ways in which the F Reorganization transaction can be used to help businesses restructure in a tax-efficient manner and provide some practical insights into completing an F Reorganization.

F Reorganization Requirements

While its definition in the I.R.C. may seem simplistic, there are certain technical rules that must be followed for the mere change to qualify as a tax-free F Reorganization. Under the Treasury regulations, an F Reorganization begins when an existing corporation (“Transferor Corporation”) transfers (or is deemed to transfer) its assets to another corporation (“Resulting Corporation”) and ends when the Transferor Corporation has (i) distributed (or is deemed to distribute) to its shareholders the consideration it receives (or is deemed to receive) from the Resulting Corporation and (ii) completely liquidated for federal income tax purposes.

The Treasury regulations set forth six requirements for a reorganization to qualify as a tax-free reorganization.

1. Resulting Corporation stock distributed in exchange for Transferor Corporation stock.

- Immediately after the reorganization, all of the issued and outstanding stock of the Resulting Corporation must be distributed to the shareholders of the Transferor Corporation.

- The IRS will disregard a de minimis amount of Resulting Corporation stock owned by anyone other than the Transferor Corporation shareholders, if necessary to facilitate the organization of the Resulting Corporation. The regulations do not expressly define “de minimis” but an example in the regulations suggests that the issuance of 1% of the shares of the Resulting Corporation to another shareholder would be acceptable.[2]

2. Identity of stock ownership.

- The same person(s) must own all of the stock of Transferor Corporation (immediately before the transaction) and all of the stock of the Resulting Corporation (immediately after the transaction) in identical proportions.

- This rule is limited by the de minimis exception identified above.

- This rule is also not violated if certain stockholders receive shares with different governance rights (e.g., voting or non-voting shares) as part of the exchange. However, the different classes of shares must be of equivalent value.

- Also, this rule is not violated if the shareholders receive a distribution of money or other property from the Transferor Corporation or Resulting Corporation, whether or not in exchange for their shares.

3. Prior assets or attributes of Resulting Corporation.

- The Resulting Corporation may not have any tax attributes (e., income or losses) or any assets prior to the reorganization.

- There is an exception to this rule that allows (i) a de minimis amount of assets to facilitate its organization and maintain its legal existence, (ii) tax attributes related to holding those assets, and (iii) holding the proceeds of borrowings in connection with the reorganization.

- Based on this rule, when performing an F Reorganization, businesses should create a new entity to ensure that there is no history of unwanted assets or tax attributes.

4. Liquidation of Transferor Corporation.

- The Transferor Corporation must completely liquidate for federal income tax purposes.

- This does not mean that the business is required to dissolve entirely under state law. Instead, it may maintain its legal existence as a separate entity. This can be one of the attractive features of an F Reorganization because the assets can continue to be held by the Transferor Corporation (with no transfer of title).

5. Resulting Corporation is the only acquiring corporation.

- Immediately after the transaction, only the Resulting Corporation may hold the property of the Transferor Corporation if the Resulting Corporation acquires the tax attributes (under I.R.C. § 381) of the Transferor Corporation.

6. Transferor Corporation is the only acquired corporation.

- Immediately after the transaction, the Resulting Corporation may not hold any property acquired from any corporation other than the Transferor Corporation if the Resulting Corporation acquires the tax attributes (under I.R.C. § 381) of the Transferor Corporation.

- These final two requirements (5 and 6) ensure that only the Resulting Corporation holds the tax attributes of the Transferor Corporation (and no other corporation) immediately after the transaction is complete.

F Reorganization Transaction Structure

The structure of an F Reorganization can take many shapes. A list of examples is set out in Treas. Reg. § 1.368–2(m)(4). Many of these structures involve mergers among related entities and/or the reincorporation of a business in a new state.[3] In practice, F Reorganizations typically involve S corporations, either as a target entity in an acquisition or as the acquiring entity. The pass-through tax treatment of an S corporation is attractive, but limits on who can be shareholders and being limited to having a single class of stock can create obstacles to retaining pass-through tax treatment for business operations.

One common way of completing an F Reorganization is through the creation of a new corporation, which initially becomes the parent holding company of a new entity that will operate the existing business. The parent holding company then sells part or all of its interest in the new entity. Structuring an F Reorganization in that manner will be the focus of the remainder of this article.

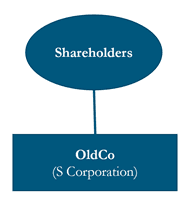

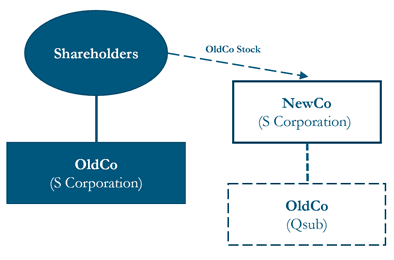

Below is a simplified diagram of the steps involved in completing an F Reorganization with an S corporation.[4]

Pre-transaction Structure

Individual shareholders own all of the issued and outstanding equity of the existing corporation (“OldCo”).

- Step 1: Formation of new corporation (“NewCo”).

- Step 2: All OldCo shareholders contribute all of their shares of OldCo to NewCo in exchange for all of the issued and outstanding shares of NewCo stock. Typically, NewCo elects to treat OldCo as a qualified subchapter S subsidiary (“Qsub”), thereby causing OldCo to become a disregarded entity for federal income tax purposes.

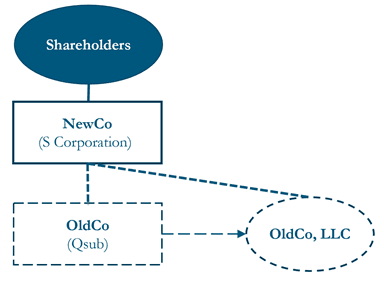

- Step 3: OldCo converts into a limited liability company under state law or merges with a newly formed LLC subsidiary of NewCo (and remains a disregarded entity for federal income tax purposes).

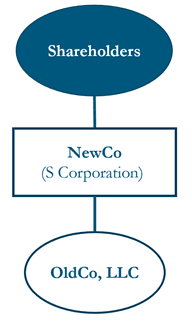

Post-transaction Structure

Individual shareholders own all the issued and outstanding equity of NewCo in the same proportion that they owned their equity in OldCo. NewCo is the single member of OldCo, LLC.

Compliance Issues

When performing the F Reorganization structure outlined above involving S corporations, one must be mindful of the tax compliance issues and impact on compliance filings moving forward.

Employer Identification Numbers

The Resulting Corporation (NewCo in the example above), must obtain its own taxpayer ID number (employer identification number (EIN)) by filing a Form SS-4. The Transferor Corporation (OldCo) would retain its historic EIN number after the Qsub election is filed.[5] As a Qsub and later a single-member LLC, unless a special election is made, the entity will be deemed disregarded from its owner for federal income tax purposes. However, there may be certain non-income tax and business reasons why the Transferor Corporation would still need to use its own EIN, such as banking relationships, employment tax filings, and contractual requirements.[6]

Moreover, even if OldCo, LLC’s classification as a disregarded entity changes so that it is recognized as a separate entity for federal tax purposes, OldCo, LLC would continue to utilize its old EIN number that it had prior to having a single owner.[7] In other words, the EIN of the Transferor Corporation will survive despite its conversion to an LLC and even after it becomes classified as a partnership or other entity (as may be the case in an equity rollover transaction).

Qsub Election Timing

Also, after Step 2 in the diagram above, it is common, and maybe prudent, for NewCo to file a Qsub election (Form 8869) for OldCo before converting OldCo to an LLC under state law (Step 3). The reason for this sequential timing is that the Qsub election must be made while OldCo is still a corporation and meets the requirements for being a Qsub under I.R.C. § 1361(B)(3)(A) and (B).

Even though the Qsub election may be made retroactive to a date when OldCo was a corporation, if it is filed when OldCo has already become an LLC and is no longer a corporation, there is risk that the Qsub election would be deemed ineffective. This risk can be misunderstood and confusing because the instructions to Form 8869 (Revised 12/2020) allow for a Qsub election to be made effective up to two months and 15 days after the date the election was filed.

This timing issue was analyzed by the IRS in Private Letter Ruling (“PLR”) 201724013. In this situation, the taxpayer had its steps out of order and submitted a Qsub election after the subsidiary corporation had converted to an LLC under state law. The IRS ruled that the election to treat the sub as a Qsub was ineffective because the corporation did not meet all the requirements for a Qsub at the time the election was made and for all periods for which the election was to be effective. Ultimately, the IRS granted the taxpayer relief because the circumstances resulting in the ineffectiveness of the Qsub election were inadvertent within the meaning of I.R.C. § 1362(f).[8]

However, if a taxpayer were to perform an F Reorganization but forgot to file a Qsub election or did not file one on time, there are certain arguments that one could make. For instance, one could argue that failure to make a timely Qsub election was inadvertent and the taxpayer deserves relief under I.R.C. § 1362(f). More significantly, the Treasury regulations governing F Reorganizations that are effective for transactions after September 21, 2015, provide an example (Example 5) of an F Reorganization transaction with a structure that indicates a Qsub election may not be needed if the plan was to convert OldCo to an LLC and the conversion occurred right after the shares of OldCo were contributed to NewCo. Under the regulations, such a transaction structure qualifies as a tax-free F Reorganization without reference to the need to file a Qsub election.

That said, cautious taxpayers and advisors may still want to have NewCo make a Qsub election for OldCo while OldCo is still a corporation and before it has been converted to an LLC. PLR 201724013 specifically stated that the Qsub election was ineffective in a case when a Qsub election is made for an entity that is not a corporation when the Qsub election was made — even if the effective date of the election is retroactive to a date when the entity was a corporation. Plus, taxpayers should not rely on the leniency granted by the IRS in that case because PLRs are expressly limited to the one taxpayer’s facts and are not to be cited as precedent.[9] If the F Reorganization is done in a short window of sequential steps, it would be prudent to make sure OldCo is a corporation on the date the Qsub election is filed, i.e., the date the election is mailed and that adequate proof of the date of mailing the election is retained. It would be advisable to send the election form in by certified mail so that you could prove submission was made on that specific date if that were ever challenged.

It may be the case that PLR 201724013 addressed a time period before the effective date of the F Reorganization regulations discussed above, and there is no need to make a Qsub election as an interim step before converting OldCo to an LLC. To avoid any problems, however, follow the steps and sequence outlined above.

Future Income Tax Filings

Beginning in the year of the F Reorganization, all future income tax filings must be made by the Resulting Corporation using its new EIN number.[10] From an income tax perspective, the NewCo will be treated just as OldCo would have been treated if there had been no reorganization, including succeeding to the S election previously made by OldCo.[11] The taxable year for OldCo will not end on the date of the reorganization; instead, all the tax attributes of OldCo will become tax attributes of NewCo.[12] OldCo would not need to file its own separate income tax return in the year of reorganization and the years following, until there is another change in circumstance that would trigger a filing obligation. Remember, in essence, NewCo and OldCo are the same entity for tax purposes.

To properly notify the IRS that an F Reorganization has occurred in a given year, the NewCo should file a statement pursuant to Treas. Reg. § 1.368-3 with its federal income tax return. This statement must include the names and EINs of the parties involved, date of the reorganization, and the value and basis of the assets of OldCo, among other items.

Using an F Reorganization to Accomplish Tax Planning Goals

While there are certainly others, here are several examples of where F Reorganizations can be a useful planning technique.

1. Enabling the sale of an LLC interest as opposed to S corporation stock.

Performing an F Reorganization prior to the sale of a business owned by an S corporation can enable the seller to sell a subsidiary single member LLC interest, not the corporate stock directly. By purchasing a single member LLC interest, the buyer would receive a step up in basis in all of the assets held by the LLC at the time of purchase.[13] Moreover, by purchasing the entire equity interest outright, there may be less of a legal and compliance burden as far as obtaining third-party consents for transferring assets. Further, buyers of an LLC interest would not need to worry about the limitations associated with owning S corporation stock. Subchapter S of the I.R.C. has strict rules for who can be an S corporation shareholder (e.g., no more than 100 shareholders, no foreign persons, no regarded entities, and only certain trusts).

2. Facilitating new equity investments from investors that would otherwise be disqualified S corporation shareholders.

As mentioned above, S corporations restrict who can be shareholders. For example, corporations and entities classified as partnerships for tax purposes cannot be S corporation shareholders, nor can foreign persons and certain trusts. As businesses scale up and take on new investors, they may want to issue equity to new investors who would be ineligible to own shares in an S corporation. Performing an F Reorganization can be a useful way to bring on those investors and retain pass-through tax treatment. After an F Reorganization is complete, the LLC subsidiary could issue equity interests in exchange for cash to those investors, or NewCo could sell a portion of OldCo and distribute the sales proceeds to its shareholders. OldCo would be classified as a partnership for tax purposes, and NewCo would retain its status as an S corporation.

3. Implementing a rollover equity transaction.

Equity rollover transactions are popular methods for keeping past shareholders and owners invested in the future success of a business even after a significant portion of the business is sold. Target corporations can first perform an F Reorganization, then allow some of S corporation shareholders to retain shares of the S corporation as a means of rolling over their equity on a tax-free basis. This is more tax-efficient than having all shareholders sell all of their shares in NewCo (or OldCo) (and trigger gain) before reinvesting a portion of the proceeds in the acquiror.[14] Another possibility would be for OldCo to issue profits interests to key employees of NewCo.

4. Selling less than all the assets of a business.

Sometimes sellers want to sell a part of their business but keep other parts. For example, if a business were to own a chain of restaurants, but the owner only wanted to sell restaurants located in state A and keep the restaurants located in state B. In this scenario, NewCo and OldCo could perform an F Reorganization similar to the one outlined above, then OldCo would distribute its restaurant assets located in state B to NewCo. As a result, all of the state B restaurants would be retained in NewCo, and the state A restaurants would be housed in OldCo. NewCo could then sell OldCo to the buyer.

5. Facilitating a corporate freeze structure.

The corporate freeze is a term used when a corporation creates at least two tiers of shares (preferred and common), but the upside value of the business is mainly held by one of the classes. In a typical freeze structure, the value of the preferred shares is limited to a liquidation preference and a modest annual rate of return. The upside value of the corporation is then housed in the common shares. In this way, the preferred interest is deemed to be “frozen.” (The same concept can be applied in the LLC or partnership context with the issuance of preferred units.) The F Reorganization can facilitate a freeze when you have an existing corporation by creating a two-tier structure where a corporation owns the preferred shares or units of a subsidiary corporation or LLC, and then new common shares or units are issued to new owners/investors in the subsidiary. [15] See our article “Exploring the Benefits of the Corporate Freeze Transaction” for a detailed discussion on this topic.

6. Restructuring an S corporation to enable the issuance of C corporation stock that might qualify as qualified small business stock under § 1202.

I.R.C. § 1202 has become a popular topic for many small businesses and startups in recent years because of the immense value it can bring to owners of qualified small business stock (“QSBS”) in the form of a capital gain exclusion. One common problem that investors run into with § 1202 is the requirement that only domestic C corporations can issue QSBS. S corporation shareholders cannot merely terminate the S election in the hope that their former S corporation stock will qualify as QSBS; there is a requirement that the corporation issuing QSBS must be a C corporation, not only at the time QSBS is issued but also at all times during the taxpayer’s QSBS holding period.[16]

To change what was once an S corporation into a C corporation interest that can issue QSBS, a company might consider undergoing an F Reorganization followed by the contribution of the single member LLC interest to a C corporation in a tax-free 351 transaction. When the dust settles, there would be a three-tiered structure of the S corporation (parent) owning shares of a C corporation (sub) owning a single member LLC interest. The S corporation would be the shareholder of the QSBS.[17] See our article on S corporations and Section 1202 for a detailed discussion on this topic and other Section 1202 topics.

Conclusion

As highlighted in this article, the F Reorganization can be a useful tool in the tax practitioner’s kit for effecting a change of entity. The F Reorganization enables restructuring to be done on a tax-free basis and it can be very valuable in pre-transaction planning. For any questions regarding F Reorganizations and other tax restructuring transactions, any attorney with Frost Brown Todd’s Tax Practice.

[1] I.R.C. § 368(a)(1)(F).

[2] Treas. Reg. § 1.368–2(m)(4) Example 3.

[3] Treas. Reg. § 1.368–2(m)(4).

[4] This transactional diagram is substantially similar to Example 5 set forth in Treas. Reg. § 1.368–2(m)(4); see also IRS Rev. Rul. 2008-18.

[5] Treas. Reg. § 301.6109-1(i); see IRS Rev. Rul. 2008-18.

[6] Treas. Reg. § 301.7701-2(c)(iv).

[7] Treas. Reg. § 301.6109-1 (h)(2)(ii); Treas. Reg. § 301.6109-1(i)(3).

[8] PLR 201724013.

[9] See PLR 201724013 (“This ruling is directed only to the taxpayer that requested it. § 6110(k)(3) of the Code provides that it may not be used or cited as precedent.”).

[10] Treas. Reg. § 301.6109-1.

[11] Rev. Rul. 2008-18; Rev. Rul. 64-250.

[12] Treas. Reg. § 381(b)-1.

[13] IRS Rev. Rul. 99-5.

[14] For more information on equity rollover transactions, see https://frostbrowntodd.com/rollover-equity-transactions/#a2.

[15] For more information on corporate freeze transactions, see https://frostbrowntodd.com/exploring-the-benefits-of-the-corporate-freeze-transaction/.

[16] I.R.C. § 1202(c).

[17] For more information, see https://frostbrowntodd.com/section-1202-and-s-corporations/.